The Trap of Elite Incomes

how capitalism seduces the ambitious from humble backgrounds

A few of you know about my day job advising fast-growing consumer brands on strategy. Occasionally, I stumble on an observation in my business highlighting important structural features of American society.

I want to share one of those with you today. In this case, it’s about our dearest friends in the 1%.

Most fast-growing consumer brands (e.g., Beyond Meat) you read about in USA Today, CNN, CNBC, or Entrepreneur magazine, rely on large infusions of investor capital to fund a rapid pace of growth. I won’t bore you with the balance sheet math, but gross profits alone do not usually allow these companies to scale in 2-4 years. The math isn’t there.

The money for venture capital investments comes from Wall Street. Your 401K money is funding venture capital indirectly by making money for investment banks. The idea is that public money benefits from betting on fast-growing privately held innovations that can operate without the scrutiny and expectations of a general firm.

Investment Banking’s Great Irony

I have noticed two very intriguing facts related to investment banking’s relationship to the startup world, which, when understood, throws light on how extremely elite compensation becomes a rigid psychosocial trap for some of the 1%:

Young investment banking associates have become a major source of startup founders. They don’t like their jobs. The work environments are 80+ hour work weeks with demanding bosses calling on you at all hours about anything. It’s a ten-year hazing process for which you are indeed paid redonkulous salaries at such a young age. Think of Jeff Bezos departing D.E. Shaw in 1994.

Executives in investment banking rarely leave that position to do anything other than become angel investors or start up their own investment firms (in the private sector) or retire. I’ve never seen any I-banking executive condescend to become a startup founder in my consumer packaged goods industry. In fact, I know one who did it for three years (mainly to learn from the trenches) and then went right back to an I-banking salary. LOL. Jeff Bezos is the one ‘executive’ who did this, but I’ll explain why he doesn’t fit the pattern in a bit.

In other words, if you are the kind of person attracted to “making partner” at an I-bank, you will forever be a committed investor and financial alchemist. Why? Well, even if you’re bored to death with this kind of work when you get to this level of remuneration, your pseudo-aristocratic lifestyle now depends on it. And there is no other way for you to make that kind of money again. Anywhere else. Right away.

How much money are we talking about? Millions a year in salary and bonuses.

When you are a 24-year-old I-banking associate earning $250K, you feel well off, but…you are not living like the 1% yet, far from it. You can step off the escalator without your entire lifestyle imploding. It will change but not implode. You are young enough to classify a few high-earning years as an aberration.

Not true for the I-bank executive who takes a fall from grace or who (rarely) quits in a huff or because of burn-out. I am NOT here to play violins for ‘suffering’ I-bankers. Hell, no. But I want to describe the ‘fall’ so middle-class people can objectively understand the privilege level here. In very concrete terms, devoid of the usual stone-throwing.

An I-Banking Executive’s Fall

In the research for my upcoming book, I found myself deep in an interview with a woman who had married an I-banking executive. At their peak income in the 2000s, he earned $1M+ annually, not including large bonuses. This unbelievable amount of income allowed them to do things like the following (I’m fictionalizing a real scenario relayed to me):

Wife: Hey, do you want to go to Miami for the weekend? (on Thursday night)

Husband: Sure, let’s do the Four Seasons this time. I might take a meeting on Saturday if we’re there. Super short, I promise.

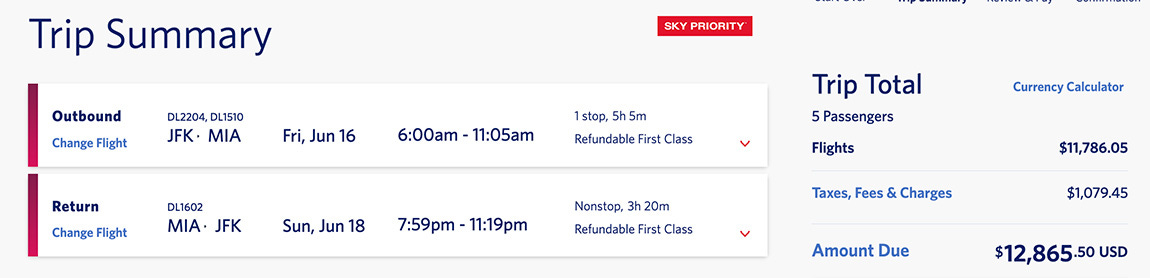

And then, the parents plus three kids would fly first class (at the highest, last-minute fare class). Refundable first class is the top Fare Class in the US air market. It’s what you have left when you book in the last 48 hours. Here’s the cost of their weekend getaway airfare today:

Two bay view suites at the Four Seasons Miami for two nights (one for a private meeting if the client is available), a total of 3,000 square feet for five plus in-room breakfast - $12,898.

This random ‘weekend’ trip totals about - $30K all in.

As my guide to the 1% made it clear in our interview, neither she nor her husband ever paused to think about what this was costing them. They never budgeted these trips. They picked precisely what they wanted. And they wanted top-shelf everything.

Never calculating the total cost of anything. This is the best way I can describe the lifestyle of the 1%.

You won’t find the 1% adjusting search filters on www.kayak.com.

When you earn this much, you spend as you wish on 99% of items, except real estate or a large yacht. Cars, RVs, trucks, ATVs, mortgages, clothing, furniture, travel, hotels, and food are items you don’t plan the expenditure on or regret later. It just happens. Money flows. Things accumulate. You will also qualify for almost any kind of mortgage you can imagine on multiple homes.

It’s the modern equivalent of aristocratic living - aristocracy lite fueled on loads of debt your crazy high income can support. Bankers are THE best at maximizing the banking system’s advantages. Shocking!

And when you lose this kind of income, you fall into a middle-class existence you had forgotten entirely about. You lose homes, cars, and boats in less than a year. The impulsive vacations cease.

The result for the woman I interviewed was a now very tenuous marriage since her husband lost his executive I-banking job in the 2008 financial crisis. Ever since then he has only made a low six-figure income as a ‘consultant’. These individuals have what is known as a poisoned resume - linked to one of the failed banks in New York. Luckily for their children, they were very young when their income peaked. They have only faint memories of that lifestyle and are happily adjusted to the normal one they now have. Phew!

Today, they think about purchases all the time, like the rest of us. She described her husband as depressed. Many of their former friends’ marriages ended with losing the 1% lifestyle. That’s what happens when your lifestyle gets down-graded that dramatically and that quickly. It breaks relationships wide open. Because the relationship either began on the premise of the aristocratic Gatsby-esque lifestyle or became dependent on it to continue. Shopping more than love was sustaining it.

These folks sound painfully materialistic to many of you, I’m sure. In the investment banking world, though, there are two tribes: the inherited rich who continue in banking and a much larger group who are extreme social climbers. Banking is their portal to riches. It is their bureaucratically managed gold mining claim.

Bear Stearns was perhaps the most extreme bank in deliberately recruiting kids from ordinary middle-class backgrounds and sucking them inexorably into an escalator of riches and opulence that would psychically entrap them as feverishly loyal to the bank. Loyal enough to take unethical risks with depositors’ money in CDS instruments.

“So there was a cultural saying that they liked to hire people who were PSDs — poor, smart and had a deep desire to be rich.”1

This culture continues today at many banks because the salaries offered still tempt highly ambitious college graduates from ordinary backgrounds. I suspect these are kids unusually exposed to parental squabbling, even violence, over everyday money issues at home. This kind of bickering not only leads to divorce, but it is the crucible of American greed: the burning desire to obtain a lifestyle so comfortable that these fights never happen. This is the most charitable understanding I can offer you for the greed you’ll see among young investment banking ‘kids.’

If you want to see a unique, searing portrayal of what this looks and feels like and how the I-banking world goads ambitious kids into a nakedly unethical, even sociopathic, pursuit of wealth, please watch the British series - Industry- on Max.

The I-Banking Refugees Are Rich Kids

Ok, maybe not all rich, but definitely kids from upper-middle-class homes like mine, where Dad (or Mom) was a highly-paid professional.

So, I noticed a pattern when I started looking into the backgrounds of 20-something refugees from I-banking. Most came from upper-middle-class or outright wealthy families. One, a client of mine, is the son of a billionaire immigrant entrepreneur. Jeff Bezos had parents wealthy enough to give him $245K as seed money for Amazon in 1994.2

Coming from childhood affluence allows young professionals the economic context in which to perceive a broader set of lifestyle choices than a social-climbing middle-class I-banking associate.

The comfort of affluence in childhood that folks like Bezos and I experienced is the comfort of not knowing financial insecurity, not having inbuilt anxiety over preserving cash, the conditions of possibility to take risks with your income in the short term, knowing full well that you can always get an ordinary job again if you run out of cash.

I did it in 2017 when I started my solopreneur consulting business with a $50K home equity loan as the emergency parachute. Jeff Bezos did it even better with a large wad of seed cash from his parents plus multiple years of I-banking income before having kids.

Increasingly, I-banking is losing the children of affluence to startup ventures. I know of at least ten such people in my specific industry alone. I admire their willingness to walk away from the escalator, but it’s also a massive sign of privilege to be able to do this. And they all know it, deep inside.

It’s very hard for a kid from humble beginnings to walk away from this kind of escalator, very hard. We should empathize with the dangers of this seduction, even if we do not want to hang out with these individuals ourselves.

This is an early draft of material appearing in my forthcoming book - Our Worst Strength

https://www.marketplace.org/2018/03/14/bear-stearns-work-culture/

https://www.scmp.com/magazines/style/celebrity/article/3188951/meet-jeff-bezos-billionaire-parents-jacklyn-and-miguel

The only solution is to value free time over what money can buy and that is VERY unlikely to happen.

When I left I banking, my choice was to return to it or go into crime. That was the only way I could replicate the income. I chose a simple life. Very hard to do.